Test Owner

The answer to this question is a definitive yes! this pandemic has brought some amazing opportunities for everyone, it has opportunities for you to progress in your career and achieve the goals you intended to achieve.

There are four things you need to consider when you decide to have a career change, we will talk about each of them below.

The financial strength of the organization you want to join

This is one of the first things you do before joining any organization you check the organization's financials. especially their financial position before the covid-19 pandemic era. check out the companies' accounts online, company checks, etc. Anything you can find on the company’s financials.

Check out if the company is investing or cutting costs? All you are trying to do is to know if the company is financially stable or not. The goal is to know if the company financials are good enough to ride out a recession.

It is not limited to your research alone, even during the interview, ask your future employer questions to know how the recent events have affected the company's financial position and their plans.

Will the series of lockdowns affect the correct functioning of the company?

It is no news that the series of lockdowns had bad effects on different sectors of the economy, these sectors include hospitality, leisure, travel, and property. The lockdown prevents people from participating in activities that would boost these sectors.

But sectors like technology, financial services, and online retailing have had a little negative impact. The lockdown has given them a lot more positive impacts as they have a lot more customers now that rely on these sectors for most of their day-to-day activity during and after lockdowns.

You need to be cautious of the sector you want to move to because if it is a sector that is negatively affected by the lockdowns depending on the degree of effect, it would be a bad idea to venture into such sectors.

What kind of role would I be playing in the company? A business-critical role, revenue-generating role, or a luxury to the organization?

The kind of role you play in the organization matter a lot if your role in the organization is critical to the running of the day-to-day activities. Then the company will continually need your skills and experience. This is great as this would make you a valuable asset to the company.

On the order hand, if you are joining the organization in a revenue-generating capacity, you need to be sure your skill sets would be able to carry out such duty without disappointing the organization. You need to consider the pandemic and other external factors that might hinder your performance.

if your role is not business-critical or revenue-generating, and it is not essential to the company's core function then the probability of you being laid off during any recession is very high, as the organization would be trying to cut down costs.

You compare the new opportunity in the new organization and that of your current role in your organization?

Before considering new opportunities, you need to consider your current role and organizations. Ask yourself questions to know your true situation in your current organization.

Are you happy with your current role? Are there opportunities to progress beyond my current role in the organizations? Does my current organization value me? etc.

If your answers to this question are, Yes! Then you need to be sure if you are making the right choice to leave.

But if after answering these questions your answer is No! then you compare and consider the options you have with the one you had in your current organization.

Should I change jobs during a global pandemic?

Yes, provided the opportunity passes the four tests above. Make sure you stay open to opportunities, retain a growth mindset, and make sure the opportunities you select allow you to progress in your chosen career.

About 2900 candidates took the chartered insurance institute exam this year; it has been decided that they will all get special consideration during the marking of the exam scripts due to the exam delivery issues a lot of them faced.

So what are the issues faced by the students? For starters, the students experienced issues accessing the remote invigilation sessions. Some candidates faced issues in accessing their preferred exam centers. There were other technical issues different students faced when sitting for the exam.

The Chartered Insurance Institute has stated that they are aware of these issues. They understand how this issue would have caused stress and inconvenience for the students.

In a similar scenario in 2019, 491 candidates who faced different issues during their exam sittings were given post-examination mark adjustments.

The Covid-19 crisis did cause some delay in the schedule of the financial planning exams; the exam continued till late November this year. The financial planning exams' main sessions were taken in January, July, and October of this year. This year alone, about 32000 candidates sat for the CII exams, and the pass rate for 2020 will be published in the first quarter of next year.

Due to the need for social distancing caused by the COVID-19 pandemic, only 30% of the exam taken from the beginning of this year to late November had remote invigilation.

70% of the multiple-choice exams were taken with remote invigilation from mid-august to late November.

During an Interview with money marketing, the Chartered insurance institute chief customer officer, Gill white, said that session-based candidates who had issues during their exams were contacted to talk about their problems. Some were offered free resits.

She also said the CII has and will continue reviewing any multiple-choice question candidate who had issues sitting for the exam and has contacted them.

All these cases are treated differently, and free resits are only offered to appropriate cases. The CII noted that pass rates vary from unit to unit, but most of the results for July and October beat the average expectations of the body.

Talking to the money marketing, about the remote invigilation process this year. Gill White said the remote invigilation has helped to promote the relationship between CII candidates and CII members. It has allowed the smooth running of the exam proceedings allowing insurance and personal finance professionals to continue their studies by allowing the smooth process of obtaining qualifications during the covid-19 pandemic.

She adds that the remote invigilation system is still far from perfect. This year CII conducted on-screen invigilation using the new CII assessment center and remote invigilation provider PSI. However, they have gotten mixed feedback on the system. CII continues to try to better the system for better delivery in future examinations.

CII is working to resolve all the issues encountered since the march exam session when the PSI system was launched. To make the PSI performance better in the near future.

CII is planning additional session-based exams in the first quarter of 2021. They are improving the overall user experience, improving the communications systems, and the booking process.

The 2021 exams will have limited physical centers and would also support remote invigilation. Gill white ended by saying the CII continues to work to better user experience for the multiple-choice exams.

RPI TO BE REFORMED IN 2030

The Retail Prices Index (RPI) will be reformed and aligned with the housing cost-based version of the Consumer Prices Index, known as CPIH, by 2030, the Treasury has confirmed.

As part of the Comprehensive Spending Review today (25 November), the government announced that the methods and data sources of CPIH would be brought into RPI in February 2030, after the date of the maturity of the final specific index-linked gilt that year.

While the Treasury had consulted on making this change as early as 2025, in the response published today chancellor Rishi Sunak said he would withhold the consent necessary before 2030 in order to minimise the impact on the holders of index-linked gilts.

Nevertheless, the government has refused to offer compensation to index-linked gilt holders, noting that there would be no change to the contractual terms with RPI still being used to determine the index ratio.

As the consultation closed to responses in August, it was warned that investors could face a fall in asset values of up to £130bn depending on the breadth and pace of the reform.

The Pensions Policy Institute predicted a £60bn hit to scheme investments of a 2030 implementation date, while the Pensions and Lifetime Savings Association estimated a 17% drop in income for a man aged 65 this year if the change was made in 2025.

'Major blow'

Hymans Robertson partner Matt Davis said the decision was a "major blow for pension schemes and their members", although noted that the impact will vary significantly based on each scheme and its rules.

The government said it "keeps the occupational pensions system under review and will continue to do so", noting the particular impact on some scheme members whose benefits are pegged to RPI.

Davis said this was a "crumb of comfort" and added: "Pension schemes that have followed regulatory and industry best practice by hedging the inflation risk inherit in providing pensions are major holders of index linked gilts and other RPI-linked assets. This change means RPI-linked assets are expected to increase at a lower rate than previously anticipated, which makes them less valuable than before. The schemes that will be worst affected are likely to be those with high levels of inflation hedging and a high proportion of CPI-linked pension increases. In some cases these schemes could see a 10% fall in funding level. The Government has stated it will not offer compensation to holders of index-linked gilts which will have a huge detrimental impact.

"We expected this to have a very significant effect on investors as a whole. We estimate that the impact on the totality of index-linked gilt holders will be a loss in the region of £100bn based on past differences between RPI and CPIH. Given the vast sums of money involved we expect to see continued pressure on the government to review its decision not to compensate those due to lose out."

Insight Investment head of solution design Jos Vermeulen said he was disappointed with the government's decision, believing the approach to be inequitable. He said: "This is expected to reduce the future change in RPI from 2030 onwards by 1% per annum, effectively transferring around £100bn of value from index-linked gilt holders (largely pension funds) to the government.

"This decision has been made despite substantial concerns being raised during the 2020 consultation, from a broad range of market participants. Insight worked to raise awareness of this issue, as although we understand the statistical problems of maintaining RPI as a legacy index, we do not believe that a solution should result in large transfers of wealth.

"Another chapter in the RPI saga has drawn to a close, but with ten years until the decision is implemented, we struggle to believe that this is the final chapter, and we will continue to advocate for an equitable solution."

'Another lottery'

And while the response is in the large part expected, Society of Pension Professionals president James Riley said the variation in scheme impacts would be stark: "The outcome of the consultation is largely as expected bringing RPI in line with CPIH by 2030. This removes one of the many uncertainties hanging over pension schemes currently and, at one level, this certainty is helpful.

"However, it's yet another lottery, alongside others including GMP equalisation, that affects otherwise similar schemes and sponsors differently. Schemes' RPI assets such as index-linked gilts and inflation swaps will be adversely impacted. Will the reduction in the scheme's liabilities be greater? And then of course, there are pension scheme members, many of whom, rightly or wrongly, will receive lower pension increases than they might otherwise have expected."

Mercer partner and chief actuary Charles Cowling said it was important that schemes now sought to understand the impact: "RPI is clearly a flawed measure of inflation and replacing it to ensure future pensions are calculated fairly is the right thing to do. Unfortunately, doing so will inevitably create both winners and losers, though arguably the impact will already have been priced into the market to some extent.

"For companies and trustees it is now crucial that they seek to understand the impact on their schemes so they can explain and communicate this clearly to their members. On the investment side, there is an opportunity to review hedging programmes to make changes that might lessen the impact of the switch."

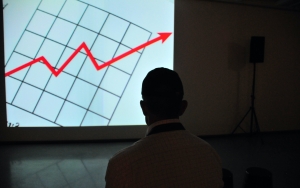

The discovery of a covid-19 vaccine should mean good news to the whole world as it means everyone and everyone gets to go back to what was once considered normal. But this return to normalcy is a blessing to some and a curse to others. Surprising right? Who would have thought that such welcomed development would be adverse to some industries and sectors, one of which is the investment asset classes?

Gold, equity, and debt funds are investment classes that may not fare very well in the wake of a normalized world. This is how the investment classes would perform and what you should do in preparation for any eventuality.

GOLD

No asset class can move in a straight line in perpetuity, and the pandemic has hugely supported the price of gold. It is only logical to expect that the price will correct and go back to what it used to be when there is no pandemic.

The price of gold hit its highest on 7th August as the pandemic raged on, but there was a decline when the announcement for the discovery of a newly approved vaccine.

EQUITY

The equity market has experienced lots of ebb and flow during the pandemic. By March it fell from a peak that was recorded in January. There has been a healthy recovery between March and August. With equity, it is expected that it will react positively to an approved vaccine's news but not for long.

The eventuality of a vaccine being released and approved for covid-19 has already factored by the market even though there is no certainty of when it will be released. Investors' advice is that investors stay true to their asset allocation if they must navigate the volatility.

DEBT

The predicted immediate response for debt investments is an increase in bond yields because central banks may not have a need to buy bonds. According to a fund managers, central banks will not quickly hike the interest rates even though they stop buying the bond yields.

It is also expected that some debt products like bank fixed deposits are expected to keep providing low-interest rates even though interest rates are not likely to rise in the near future.

The topmost priority for most governments around the world is to discover a vaccine for the coronavirus in the shortest time possible. The result of an eventual discovery and approval of a vaccine is volatility in a lot of investment asset classes. It is best that to navigate these times; you should employ and heed the advice of experts. This would help you to make sure that you invest in the appropriate products.

Since the Covid-19 pandemic, mental health and related issues have been talked about emphatically. All the rules, guidelines, and restrictions that have been stipulated, which also cause anxiety, have so much impact on our lives in ways that we could not fathom. The new working environments and situations have resulted in stress and mental exhaustion.

We all have mental health. Good mental health reflects in our daily lives. Good mental health steers us in the path of purpose and provides clarity in our directions. We even have the energy to actualize the goals that we want to actualize. When we are faced with challenges, we can meet these challenges squarely.

One thing that is always in constant flux is our mental health. It is ever-changing because some times and situations make us feel stressed or feel down. The problem with some of these negative downtimes is that it can metamorphose into mental health issues with visible effects in our day to day lives. These feelings do not just go away all the time. Mental health, just like physical health, has places where and facilities can help you keep yourself fit. Physical fitness has places with equipment, facilities, and specialists to physically help you be in the best form. This is the same with mental health. There are deliberate efforts and steps that we can take to develop and better our mental health and improve our capacity to recover quickly from difficulty. This is why the importance of self-care cannot be overemphasized. It is important to practice self-care even though it can be difficult, especially when dealing with depression, anxiety, and low self-esteem.

Some ways can help one to improve our mental health, and some of them include;

TALKING TO SOMEONE: erroneously, people consider talking to others about their feelings as a sign of weakness. This is untrue, and the opposite is the case as it means you are taking control of your wellbeing. It is advisable to talk to your co-workers or colleagues, supervisor, and friends, or family. You should speak to people that you feel comfortable with.

STAY ACTIVE: This is not limited to rigorous and planned out exercises; instead, it could merely be taking a stroll during your break to improve your self-esteem, help you focus, and aid you in feeling better.

GOOD DIET: Your mental health benefits from healthy eating as much as your physical health.

DRINKING RESPONSIBLY: excessive intake of alcohol can worsen your anxious feeling.

KEEP IN TOUCH: the effects of obesity and smoking can be likened to the impact of loneliness. It is terrible for your health. Relationships are essential in your workspace and anywhere else.

ASK FOR HELP: You are not an island, and life can be overwhelming, so it can be in your benefit to ask for help and assistance when you need it.

TAKE A BREAK: Your mental health can benefit from a change in scenery and pace. Once in a while, move away from your work desk, go to the park, pick up a book, and do things to be happy. Get enough rest and sleep too.

DO WHAT YOU ARE GOOD: AT One way to boost your self-esteem is to do something you are passionate about. Doing something that you know how to do will make you feel good about yourself.

We hope that you are staying safe and well with whatever way you choose to practice self-care.

Charities such as See Me, Scotland, Breathing space, and Samaritans have good digital facilities and resources to help you, and they are just a phone call away if you need help and are struggling.

Martin Crines at Jenson Fisher was the perfect recruitment partner for us when we recruited our new Head of Finance. He quickly got to the heart of what we needed in the role - both in terms of skills and experience and personality and attitude. He worked hard to understand our needs, our direction of travel and what I needed from the working dynamic. As a result he assembled a terrific shortlist and quite rightly predicted the person that we ultimately appointed. That appointment has been very positive with follow up support offered by Martin to both me and the newly appointed employee. I'd happily work with him again.

Nothing will communicate your value and potential to recruiters and employers more than your LinkedIn profile. In recent times, it has become a sort of CV. Knowing how important LinkedIn has become, it is important to update your data on the platform. This means you must be aware of what you need to add and what is not necessary.

It has probably been a while since you last updated the information on your profile or you don’t even have a profile in the first place. If you do not have a profile then it is a good time to create a profile. You need this digital profile to announce to interested parties of the things you can do. It is a platform that can allow you to show everyone your skills, training, and what you can bring to the table if you are hired. It is a chance for you to set yourself apart from others.

There are ten steps that you must follow to make the best of your LinkedIn profile. You must communicate to potential employers and recruiters that you are skilled in your career and that you are keen on details. It will also help if you portray yourself as a professional. You must show seriousness.

INVEST TIME

The first thing about your profile must be that it is thorough and complete. A professional profile must not look shabby as it passes a message that you can easily be distracted or that you see things through. You must have a complete profile that details your training and previous work experience. LinkedIn can help you to know how strong your profile is and can suggest how to make it better.

CREATE AN ATTENTION-GRABBING HEADLINE

You should avoid terrible headlines. Your headline on LinkedIn is where you show off your talents and potentials. It should differentiate you from other profiles. It is also an opportunity to define your vision and the type of opportunities that you want on LinkedIn.

ARE YOU EASY TO CONTACT?

If you are looking to be hired through LinkedIn then you must provide a means to contact you easily. There should be a clear and easy means of contact on your profile. You must provide an email or phone number that will be used to reach you. This not only betters your chances but it also makes you appear serious and professional.

SHOWCASE YOUR ACCOMPLISHMENTS

Blow your trumpet a little. Share your accomplishments on your profile generously. You need to do this because recruiters want to know that you have achieved things in the past. These can include your qualifications, awards, completed projects, and the professional events that you have attended.

SMILE, YOU ARE ON CAMERA

Your picture might just be the most eye-catching thing about your profile. Potential employers and recruiters can judge your personality from your picture.

EMBRACE TECHNOLOGY

You can use short videos, photos, and even PowerPoint that showcases your expertise and skills. This also indicates that you are in tune with the time and you are tech-savvy which is good for you.

IT’S NOT JUST WHAT YOU KNOW

Always share content on your profile. This helps you to show the recruiter or employer that you know what you are doing. It is a good way to let them know that you are a round peg in a round hole.

REVIEWS ARE GOOD NEWS

What good things do your colleagues and clients have to say about you? Well, you should include their praise and endorsements on your profile. Reviews and endorsements communicate that there is something valuable about you.

KEEP IT UPDATED

If you have put your profile in place then it is time for you to come up with a schedule that helps you keep your profile updated. Share articles and content, share your new experiences, and even add your new qualifications always.

The steps above are the easiest way to have a powerful LinkedIn profile that will attract recruiters and potential employers.

Of course, you can change jobs during a pandemic. In fact, it is an open window to increase the progress of your career, but before you jump into such decision, you must first consider the following;

1. Compare Your Current Company And Role To The Potential

This should be your first step before you consider leaving your current workplace. Access yourself by asking these questions;

• Do I like my job?

• Do I like this company?

• Does my current organisation value my input?

• Are there any opportunities to progress within my current workplace?

• What would my current organisation do in economic difficulties?

If 90% of the answers to the above assessment is positive, then your current workplace is the best place to be. Sometimes during recessions, what you think is the best/safest career option may turn out to be the riskiest.

2. The Financial Background Of Your Potential Workplace

The news is a great place to begin your investigation; if the company you are eyeing has got pre-COVID-19 financial problems, then it will be on the news or online. Consider the financial position of the company – is it cost-cutting or making investments?

Quick note: If then you make it to the interview, do not hesitate to ask your employer the impact of current activities on the financial status of the company. Also, inquire about the company’s plans; all these will guide you on whether the company is in a recession or financially buoyant.

3. The Impact Of A Global Lockdown On The Organisation

Though it is believed that global lockdown as a result of a pandemic can deplete the progress of a company, but some businesses flourish exceedingly in this period. Businesses that concentrate on financial services, food, online retail and technology do not feel the impact of a lockdown compare to sectors dealing with property, leisure, hospitality and travel; these sectors would suffer greatly.

Now it seems your options are limited, but businesses prone to suffering during a lockdown can pass for a potential job switch only if they pass point number two.

4. What Are The Implications Of Your Role?

The role you play in a company is vital. Do you presume your role as luxury, core function or revenue-generating?

If it is a core function role, then you should be confident the company will do their best to keep you happy even with a lockdown.

Now, if it is a revenue-generating role, the ball falls in your court. How? You have to meet the expected revenue no matter the economic condition and being a newly employed won’t get you “goodwill” anytime soon. On the other hand, if you do not fall under these two critical roles, then during a recession, you will become a luxury the company cannot afford.

Quick Conclusion

Should you change jobs during a pandemic? Yes, but do not turn a blind eye to these four points and at the same time be vigilant to a great opportun

Sadly, the coronavirus pandemic still continues with little or no success in all attempts to finding a solution. This hardly comes as a surprise. However, it is important to review and keep our business operations up to date in order to optimize our productivity.

Working remotely has one very obvious difficulty and it is the inability to have physical interactions. Working from home makes it difficult to communicate effectively. These issues will not persist for long as I am here to help you work remotely with improved communication skills.

LISTEN

Listening attentively to your colleagues is essential in communication. Employers and employees do not listen attentively when it is actually a key part of effective communication. It is difficult to communicate efficiently if you are not good at listening. Listening and communication are two peas in a pod. During communication be sure to listen attentively and also respond when necessary. You are only able to provide feedback when you have acknowledged what has been said to you.

HOLD OPEN MEETINGS

Meetings can be boring. We are always only physically present without being a part of it actually. We zone out during meetings, become lost or distracted, and even worse fall asleep. We need to be active and the best way to achieve this is to hold open meetings. In open meetings, everyone involved gets the chance to express their views and thoughts. When a meeting is interactive it helps effective communication.

COMMUNICATE WITH HUMOUR

Robotic communication is not effective communication. The clear difference between human beings and robots is the ability to exhibit emotions and be creative. You should apply this to your advantage by bringing up humour and light banter with colleagues. This is a good way to foster friendly relations with colleagues. It would also help you work better with your colleagues and improve trust since the air is friendly.

EMAIL

It is best you send confirmation emails in a bid to sustain professionalism. There are organizations that make use of social platforms such as Skype, Zoom, and even Slack but these do not communicate professionalism as much as emails. Emails are also proof of communication.

TRAINING

We all dread trainings. It is considered to be more boring than meetings. The truth is that training does not have to be boring. You should keep your employees up to date through training. You can use videos, gifs, photos, and graphics to make training more interesting. Training helps all employees get uniform information and knowledge since they learn at the same time.

SET SCHEDULED HOURS, AND STICK TO IT

It is important to fix meetings with employers and colleagues but it is even more important that you stick to time. Punctuality is important and it communicates professionalism.

ENCOURAGEMENT AND FEEDBACK

Criticise constructively. It is important to let your employees and colleagues know that you appreciate their hard work and see what they are doing. It is also equally important that you correct them and offer suggestions. You should support and encourage them with healthy feedback.

Financial advisers and their role in the distribution of funds is changing and it is changing quickly. Financial advisers were relegated to the background while single-strategy asset managers were at the fore before now. They achieved this through product sales and the influence they wielded over the advisers.

In recent times especially after the Retail Distribution Review, it became clear that advised assets were flowing to fund managers who made investment decisions on the behalf of their clients and also into multi-asset funds. This has taken the responsibilities of asset allocation and the decisions on fund selection away from financial advisers.

Not a lot of advisers embrace the fact that they have become fund pickers. They have come to rely heavily on research and consultations or fund panels to build custom-made portfolios for every one of their clients.

The Evolving Role of Advisers

Most financial advisers are heavily weighing in on the aspect of the behavioral coaching aspect of financial planning. They would rather associate with the tag of “financial planner” in place of “investment adviser” or “wealth manager”. The evolving role of financial advisers has caused a major change in the investment world.

The Influence on Advisers

The largest influence on advisers which continues to impact their roles comes from research agencies. Advisers make use of these research agencies in their advisory roles and process. This use of research agencies has led to the emergence and growing presence of big research agencies such as Morningstar and FE fundinfo.

The influence of research agencies has made it possible for a financial adviser to offer custom-made portfolios. These portfolios are fast growing because of the dependence of the financial advisers on research agencies.

These research agencies offer more than just the comparison of funds and assessment but they have gone further to help the advisers with the location of assets and the examination of the performance of Discretionary Funds Managers.

There is no mistaking the influence research agencies to have over financial advisers and their assets. Two out of three financial advisers make use of the services of research agencies for the comparison and assessment of funds.

Taking Back Influence

Asset managers must find ways to regain influence over advisers. They will remain in dire positions if they fail to do something. They keep losing their influence as long as financial advisers continue to work more with research agencies, discretionary funds managers, and their platforms.

The way for asset managers to regain influence is to find a way to establish partnerships with advisers where they provide services of risk assessment and management and back-office systems for ease in the navigation of the tough market.

Product providers may attempt to take back some of the influence through strategic acquisitions should asset managers fail to regain and exert some of the influence on advisers.